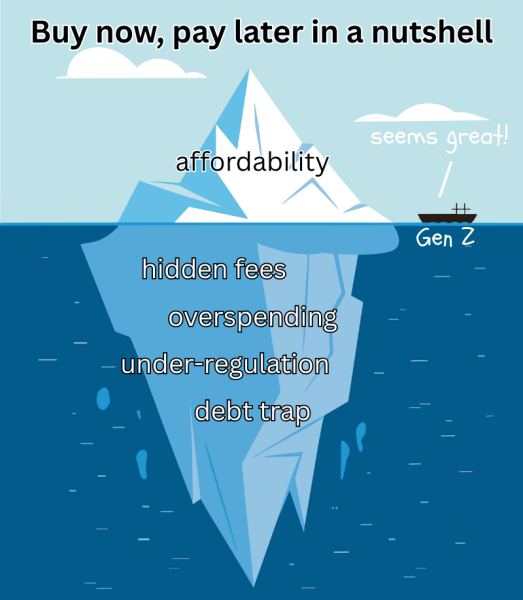

The “burrito loan” suggests that rather than paying $15 up front for a burrito, one should pay that price in four monthly payments. Originally an internet joke popularized after Klarna and DoorDash’s partnership in early 2025, this term illustrates the dangers of Buy Now, Pay Later (BNPL).

Surging in popularity during the Covid-19 pandemic, Buy Now, Pay Later payment plans are short-term loans that allow users to pay for products in small installments. Major retailers such as Amazon, Walmart, Target, eBay, Costco and Home Depot have adopted BNPL providers, the most popular of which are Klarna, Affirm and Afterpay. These companies bill BNPL as a more convenient alternative to credit cards that allow more responsible spending and greater flexibility.

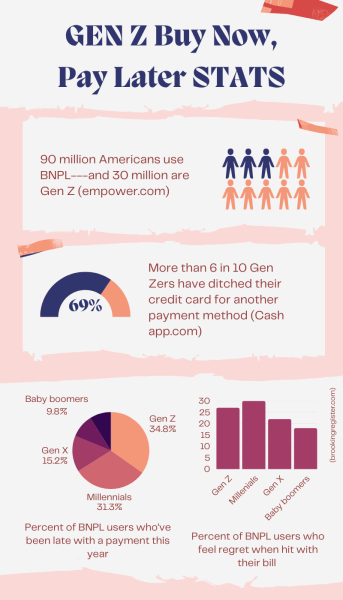

BNPL has been especially appealing to Generation Z (born 1997-2012), who really don’t like credit cards due to fear of debt and lack of understanding; 57% of Gen Z don’t understand complicated credit card terms. Providers run soft credit checks — which don’t lower credit scores, as opposed to hard checks — enticing younger shoppers who often have little or no credit history. In fact, 55% of Gen Z feel BNPL helps them manage their finances better than debit or credit cards.

However, this belief is false; BNPL creates an illusion of affordability by appealing to people’s desire for immediate gratification, which young people are especially susceptible to. People who would normally shy away from the $200 price tag on a pair of headphones find it easier to rationalize the purchase when it’s split into four $50 payments. This, according to the Federal Reserve Bank of New York, encourages overspending since customers spend 20% more when BNPL services are available.

Despite the problems with credit cards, they are the better of two evils. Yes, BNPL may offer 0% interest rates on purchases — average credit card interest rates are 20% — but loans longer than the traditional “pay-in-4” ones are harsher with rates as high as 36.99%. Additionally, on regular BNPL loans, consumers can get hit with $30 in late fees for missing a payment. The limited current regulation on BNPL compared to credit cards leads to less transparent policies and highly variable fees, which is bad news for the 39% Gen Z users who’ve been late with their payments in the past year.

Furthermore, BNPL can lead to debt-stacking, where users take out multiple loans, sometimes with different providers. In 2024, 63% of borrowers took out multiple BNPL loans, with 33% using different providers per loan.

Fair Isaac Corporation, whose credit score is used by 90% of top lenders, announced in June that their credit scores would now incorporate BNPL payments. This will positively impact responsible users of BNPL, but it’ll be yet another consequence for users who struggle to make payments on time. Poor credit scores make it harder to get approved for loans or credit cards, and can result in higher interest rates for the borrower even if approved.

While Gen Z makes up 20% of the US population, they account for a third of BNPL users. These services are inherently more attractive to young people and encourage unhealthy spending habits for a generation already struggling with debt. The good news is, Congress is currently looking at the Buy Now, Pay Later Protection Act of 2025 (HR 6891), which would apply credit card-like protections to BNPL loans. In the meantime, Gen Z should avoid these services at all costs.